Estate planning is a thoughtful process to manage and distribute your assets, ensuring your family’s financial security, reducing tax burdens, and preserving your legacy. By using tools like wills, trusts, succession planning, and charitable structures such as NGOs or Section 8 companies in India, you can create a tailored plan to meet your goals. This blog provides a comprehensive guide to these elements, enhanced with visuals, to help you secure your family’s future.

The Importance of Estate Planning

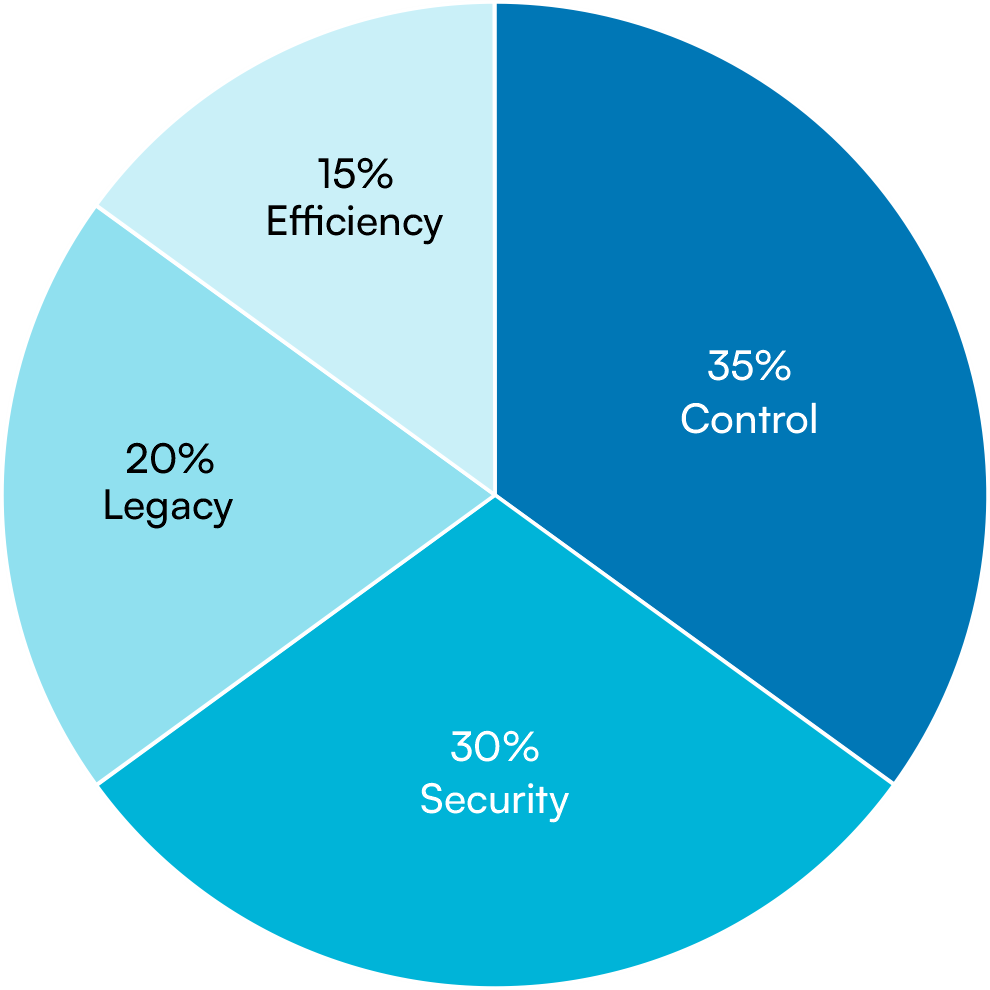

Estate planning ensures your assets—property, investments, or personal belongings—are distributed according to your wishes, protecting your loved ones and supporting causes you value. Without a plan, your estate may face lengthy legal processes, disputes, or unintended distributions under laws like the Indian Succession Act, 1925, or personal laws such as the Hindu Succession Act. Benefits include:

- Control: You decide how your assets are distributed.

- Security: Protects your family’s financial well-being.

- Legacy: Supports charitable or personal goals.

- Efficiency: Minimizes taxes and legal delays.

Wealth preservation is critical, as many families lose significant wealth across generations due to poor planning.

Why Estate Planning Matters

Core Elements of Estate Planning

1. Wills: Your Blueprint for Asset Distribution

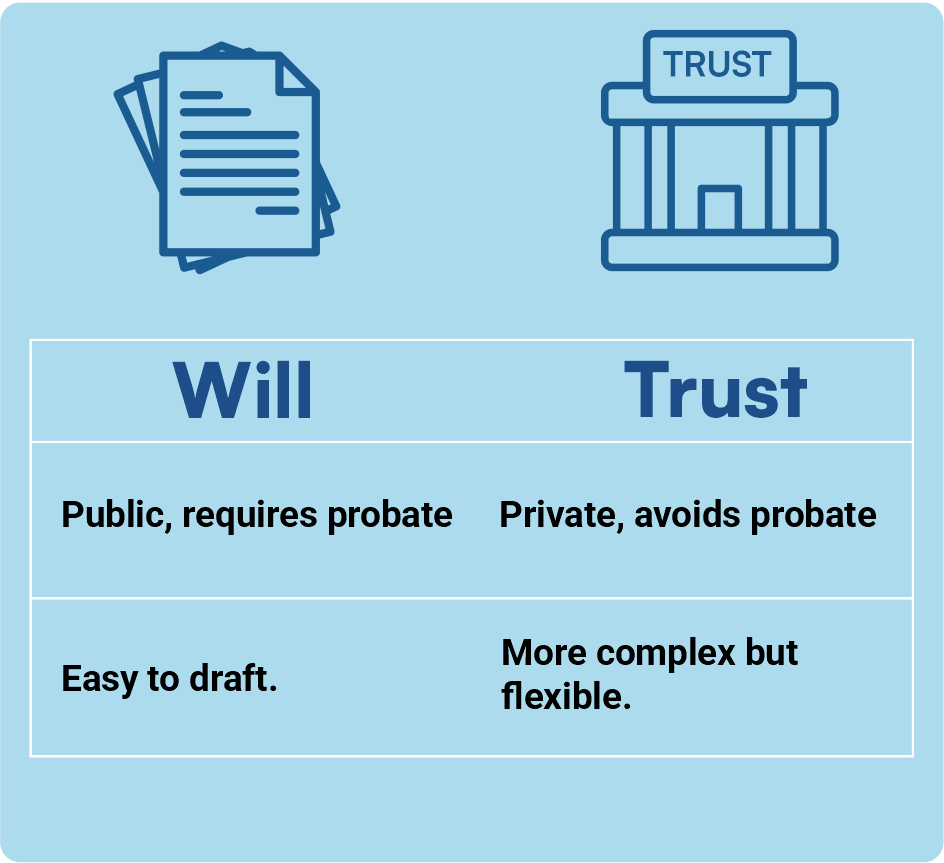

A will is a legal document that specifies how your assets should be distributed after your death. Governed by the Indian Succession Act, 1925, it’s a foundational tool for estate planning.

Key Features of a Will

- Details: Includes your intentions, beneficiary names, executor appointment, and asset distribution instructions.

- Legal Requirements: Must be signed by you and witnessed by at least two people. Registration is optional but adds authenticity.

- Probate Process: Wills require court validation (probate), which can be public and time-consuming.

Best Practices

- Write clearly to prevent misunderstandings.

- Update after life events like marriage or the birth of a child.

- Consider pairing with a trust to avoid probate delays.

Challenge: Wills alone may not suffice, as probate can delay distributions and expose details publicly.

2. Trusts: Strategic Asset Management

A trust, governed by the Indian Trusts Act, 1882, allows a trustee to manage assets for beneficiaries. Trusts offer privacy, flexibility, and tax advantages, making them a powerful estate planning tool.

Types of Trusts

- Revocable Trust: You can modify it during your lifetime; avoids probate but offers fewer tax benefits.

- Irrevocable Trust: Fixed once created; provides tax savings and protects assets from creditors.

- Testamentary Trust: Established through a will, effective after death, often for minors.

- Charitable Trust: Supports causes like education or healthcare, offering tax deductions under Section 80G.

Advantages

- Privacy: Trusts remain confidential, unlike probated wills.

- Flexibility: Set conditions, such as releasing funds when a beneficiary reaches a certain age.

- Tax Benefits: Certain trusts reduce estate or income taxes.

- Protection: Shields assets from legal claims or creditors.

Example: A business owner creates an irrevocable trust to pass company shares to their children, ensuring business continuity and reducing tax liability.

3. Succession Planning: Preserving Wealth and Leadership

Succession planning is essential for families with businesses or significant assets, ensuring smooth wealth and leadership transfer to the next generation. It’s particularly vital in India, where family businesses are prevalent but often struggle to survive beyond one generation.

Steps for Effective Succession Planning

- Choose Successors: Identify capable family members or professionals.

- Prepare Successors: Provide training and mentorship.

- Formalize the Plan: Use legal tools like trusts or shareholder agreements.

- Optimize Taxes: Utilize gift exemptions to reduce tax burdens.

- Update Regularly: Review every few years or after major changes.

Common Issues

- Family Conflicts: Emotional disputes can disrupt plans.

- Tax Challenges: Asset transfers may incur capital gains tax.

- Legal Requirements: Comply with the Companies Act, 2013, for businesses.

Scenario: A family-run textile business uses a private trust to transfer ownership to the next generation, structuring transfers to minimize taxes while maintaining control.

4. Charitable Giving: NGOs and Section 8 Companies

Incorporating philanthropy into your estate plan creates a lasting impact while offering tax benefits. In India, you can support causes through NGOs or establish a Section 8 company under the Companies Act, 2013.

NGOs in Estate Planning

- Structure: Registered as trusts (Indian Trusts Act, 1882), societies (Societies Registration Act, 1860), or Section 8 companies.

- Purpose: Fund initiatives like education, healthcare, or environmental conservation.

- Tax Incentives: Donations may qualify for deductions under Section 80G.

- Setup: Requires at least two trustees and a trust deed outlining objectives.

Section 8 Companies

These are non-profit entities focused on social welfare, education, or charity. They offer:

- Professional Structure: Operates like a company with governance standards.

- Asset Ownership: Can hold property and generate income for charitable goals.

- Tax Benefits: Eligible for exemptions under Sections 12AA and 80G.

Compliance for Section 8 Companies

- Annual Filings: Submit financial statements and returns to the Registrar of Companies (ROC).

- Board Meetings: Hold at least two per year.

- Audit: Mandatory statutory audit.

- Profit Use: Income must support charitable objectives, not distributed as dividends.

Example: An individual allocates part of their estate to a Section 8 company for community healthcare, reducing their taxable estate while creating a legacy.

Steps to Begin Estate Planning

- Inventory Assets: Document all properties, investments, and valuables.

- Set Objectives: Decide how to distribute assets and include charitable goals.

- Seek Expertise: Consult estate lawyers, financial planners, and tax advisors.

- Select Tools: Use wills, trusts, or succession plans as appropriate.

- Communicate Plans: Share with family to align expectations.

- Review Periodically: Update every 3–5 years or after significant life changes.

Mistakes to Avoid

- Delaying Planning: Risks intestate succession under personal laws.

- Self-Drafted Documents: May lack legal validity or clarity.

- Overlooking Taxes: Can lead to unexpected tax liabilities.

- Poor Communication: May cause family disputes.

- Neglecting Updates: Outdated plans can create confusion.

Conclusion

Estate planning is a vital step to secure your family’s financial future, protect your assets, and build a meaningful legacy. By integrating wills, trusts, succession planning, and charitable vehicles like NGOs or Section 8 companies, you can create a plan that reflects your values. Begin today by consulting professionals to ensure your wishes are fulfilled efficiently.

Founder

Ridhi Karan

![[⚠️ Suspicious Content] Business professionals analyzing financial charts and documents](https://ridhikaran.com/blog/wp-content/uploads/2025/05/ridhi.png)